Markets Today▲ index

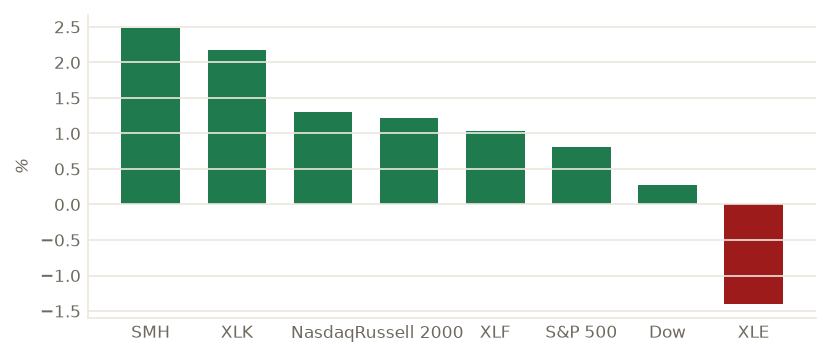

The risk bid returns as the oil premium bleeds: chips lead Thursday's tape (SMH +2.48%, measured) with the Nasdaq +1.30% to 26,206.89 and the S&P +0.81% to 7,543.64 despite fresh US strikes on Iran

Thursday inverted Wednesday yet again — this time to the upside. The US launched a new round of airstrikes against Iran early Thursday and Tehran answered with strikes on US assets in the Gulf and neighboring states, per TheStreet's session wrap, yet equities looked straight past it: the Nasdaq rose a measured 1.30% to 26,206.89, the S&P 500 0.81% to 7,543.64 and the Dow 0.27% to 52,487.41, with semiconductors (SMH +2.48%, measured) and broad tech (XLK +2.18%) leading while energy (XLE -1.40%) gave back Wednesday's gains as crude retraced. The tell is the pairing: stocks up, oil down, on a day the shooting continued — the market is trading the continuing US-Iran talks, not the strikes.

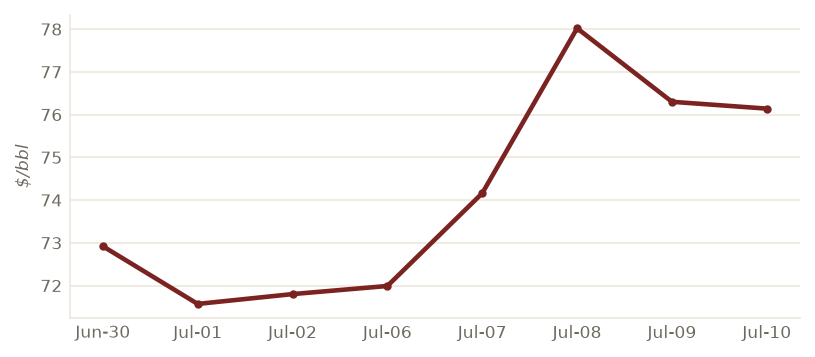

Oil gives a third of the spike back — Brent settles -2.2% at a measured $76.30 as US-Iran ‘technical talks’ continue and the week ends steadier

The Hormuz risk premium that re-armed on Wednesday started bleeding out on Thursday. Brent settled at a measured $76.30, down 2.2% from Wednesday's $78.02 spike, and the fresh Friday-morning mark reads $76.14 — Bloomberg pegs the market steadying near $76 into the weekend with WTI trading back below the mid-$70s. The reason is the diplomacy running underneath the strikes: a US official told CNBC that ‘technical talks’ with Iran are continuing and Washington remains committed to a solution, even after President Trump declared the ceasefire ‘over.’ The market's implied read: this is coercive bargaining, not a blockade — a supply-disruption tail worth a handful of dollars, not a re-run of April's ~$126 panic.

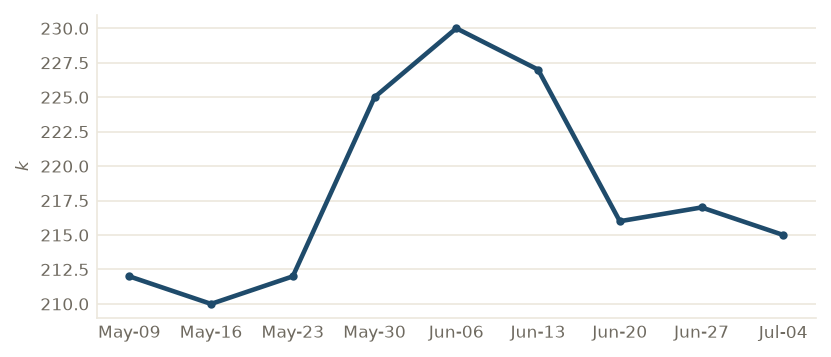

Jobless claims hold at a measured 215k (consensus 218k) — the labor market still isn't breaking, it's just not hiring

Thursday's only top-tier data point came in quiet: initial claims for the week ending Jul-04 printed a measured 215,000, down from 217,000 and below the 218,000 consensus. The fuller picture stays two-sided — continued claims sit at a measured 1.814M, the fourth straight reading at or above 1.8M, even as every 2026 week has held below 1.9M. Firings remain low; re-hiring remains slow. For a Fed whose June minutes flagged broadening inflation, a labor market that refuses to crack removes the easiest argument for cuts — which is exactly how the rates market read the week, with the 2Y at a measured 4.21% (Jul-08 mark).

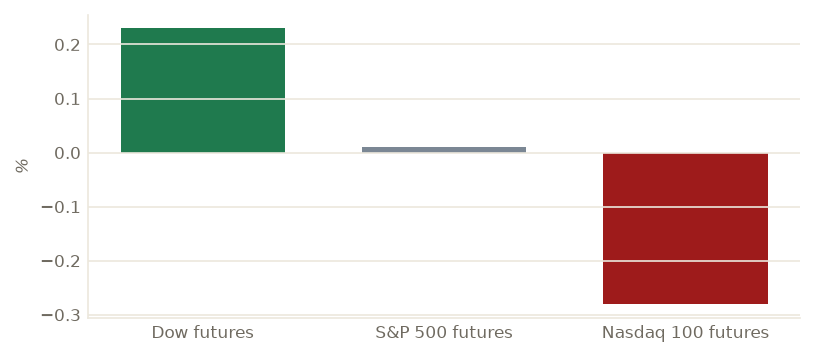

Friday's main event: SK Hynix debuts on the Nasdaq after pricing the biggest-ever foreign US IPO at $149 — futures diverge with Dow +0.2%, Nasdaq 100 -0.2%

Pre-market Friday the tape is split around a single event: SK Hynix's US listing. Dow futures were up about 0.2% while Nasdaq 100 contracts slipped 0.2% and chip stocks traded lower pre-market, per Yahoo Finance and Benzinga, as investors made room for the memory-chip maker's debut — priced Thursday night at $149 per ADS, raising $26.5bn in the largest first-time US listing by a foreign company on record. With demand reported at roughly seven times the shares offered, the open is a live-fire test of how much appetite the AI-hardware trade still has after two weeks of violent chip rotation. Beyond the IPO the calendar is empty until Tuesday's double-header: June CPI and the big-bank earnings kickoff.